Why invest in UK property today?

The last four years have been anything but straightforward for investors. From Brexit to the Covid-19 pandemic, a war in Ukraine to the current inflation-related economic volatility, financial markets have and continue to change rapidly.

How do investors react in uncertain economic times?

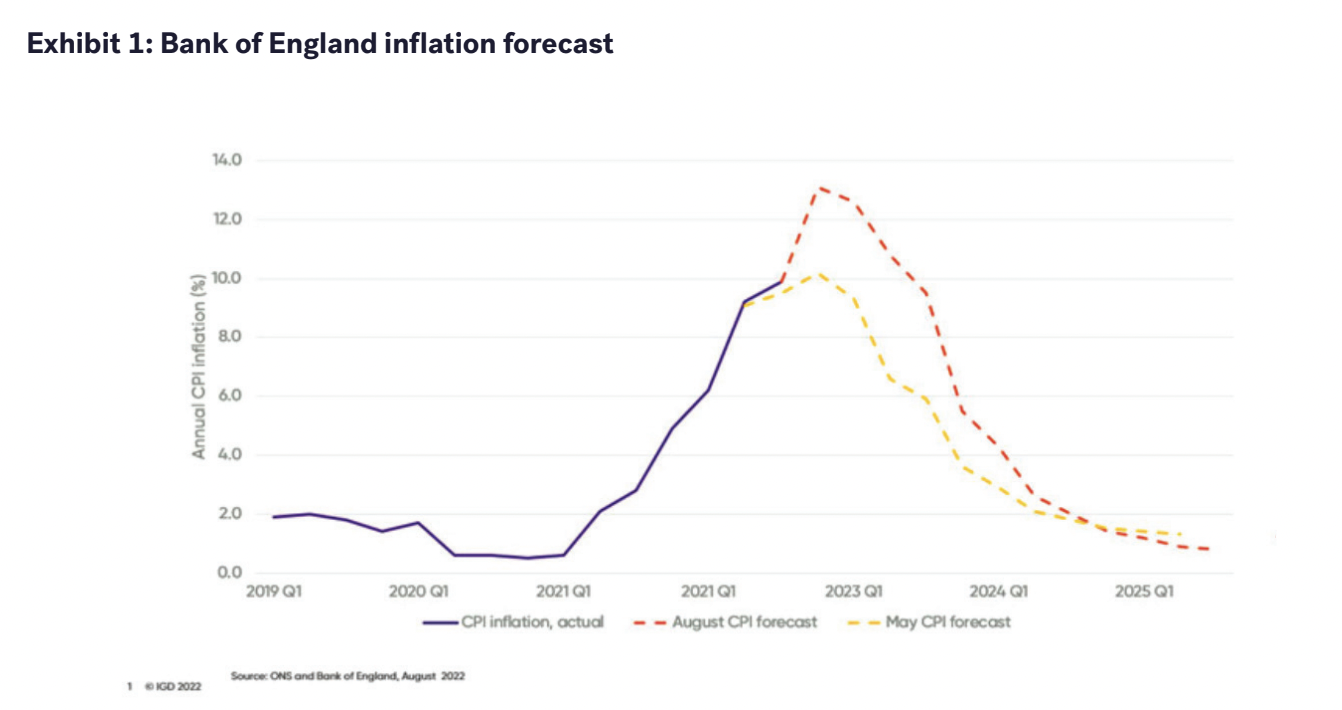

Investors don’t like uncertainty, it makes decision-making all the more difficult. Typically investors will retreat to holding cash in response to uncertainty. The current inflationary environment however, poses a unique set of challenges and opportunities. Inflation is currently at 10%, the highest it has been in the UK for 40 years. This puts a lot of pressure on holding cash savings: someone with £100k in savings would lose £10k a year in value. The issue is complicated further by the fact that we expect inflation to be over 5% for almost the next two years (see Exhibit 1), sitting on the sidelines that long with cash is an unattractive option.

So, how do investors effectively deploy their cash or readjust their asset portfolios to best meet the challenges of the macroeconomic uncertainty we face? Not all asset classes are available to mainstream investors, but let’s consider the major ones that are as property, stocks and crypto. With that in mind, let’s take a look at their performance over the last 12 months (see Exhibit 2).

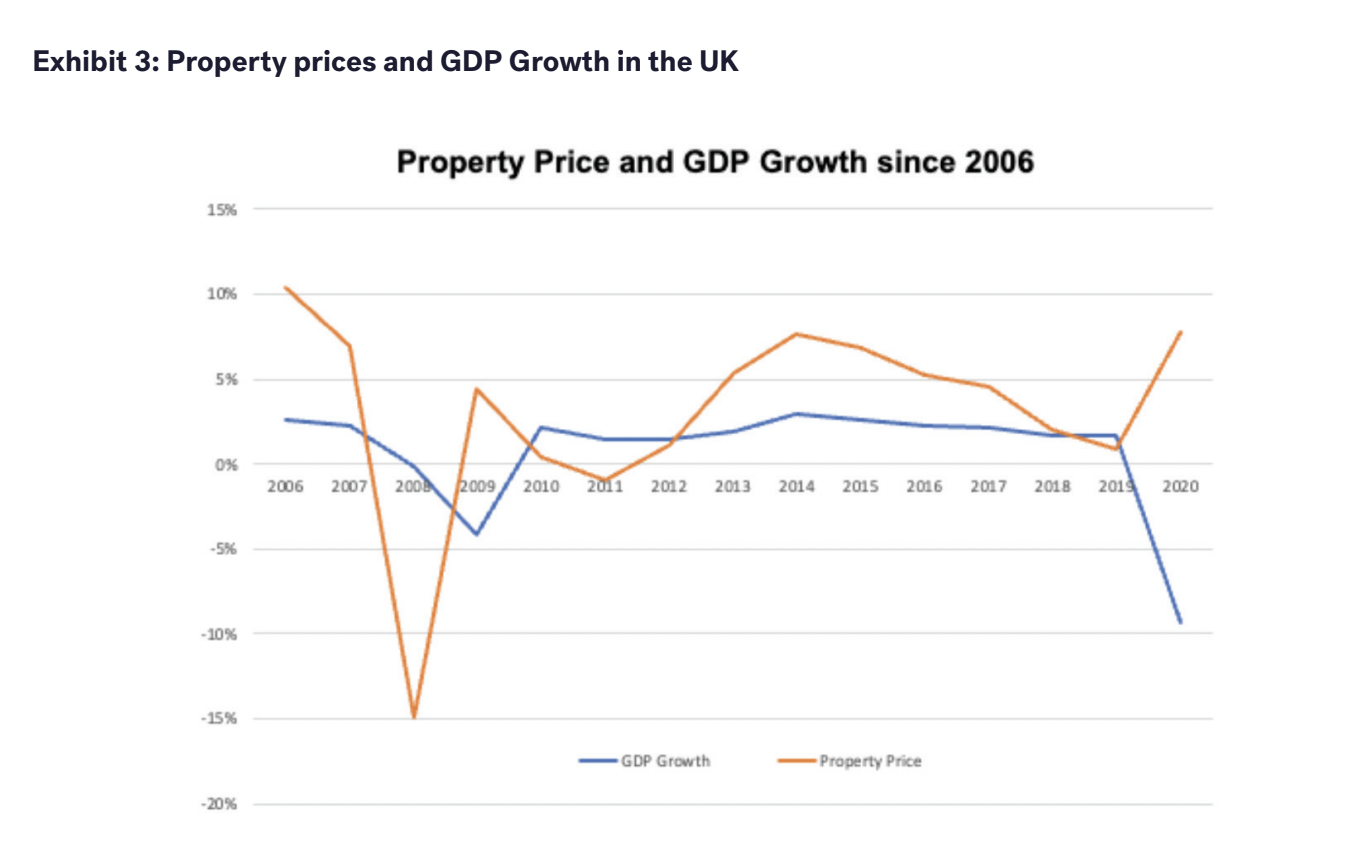

This chart uses the month on month percentage change of opening prices for stocks, and the average property price for property. The baseline for this data is October 2021. The results? Property has significantly outperformed the other asset classes in last 12 months to July 2022 (while the FTSE 250 has fallen -26%, Bitcoin -56% and Ethereum -56% over the last 12 months to October 2022). But our analysis doesn’t stop there: when looking over a longer time period to see if property prices were just as robust in other recessionary environments, the results are similarly encouraging (see Exhibit 3).

Property prices have been robust in the last three out of four recessionary environments over the last three decades (the subprime mortgage crisis was the only instance where UK property prices suffered and then recovered to grow by +5% within just 12-18 months). It is remarkable to see that consistency over such a long period and in response to such a diverse range of causes, e.g. the dot.com crisis, inflationary crisis and Covid-19 pandemic. In addition, data from the Federal Reserve Economic Data looking at the US housing market shows that investors purchasing property at the start of the dot-com bubble typically experienced 6% house price growth in the first year and over five years this figure grew to almost 50%.

Why do property prices remain robust over time?

Here are some core assertions:

Demand and supply

There is a structural mismatch between the supply of property and the demand for it in the UK. The National Housing Federation estimates that England needs 340,000 new homes every year. In 2020/21 only 216,000 new homes were built, resulting in a deficit of 124,000 homes in that year alone. This has been the case for the last decade or more, meaning the accumulated deficit is significant. What compounds the issue is that during recessions, the developer market and the building of new homes gets hit hard (e.g. due to disruptions from Covid-19, increased financing costs, material costs). So we must expect even fewer new homes in the coming years.

Property is foundational to UK financial markets

Property prices are intrinsically linked to consumer confidence. We all feel wealthier when the price of property increases. If consumer confidence falls, so does consumer spending which in turn impacts a large proportion of businesses in the economy. Property prices also underpin a large part of the UK financial system and falling prices threaten financial stability. The risks from this dual impact on consumer spending and financial stability mean that the Government will likely step in to support prices. We’ve seen this when it comes to Stamp Duty: in 2021 and most recently announced in the September 2022 mini-budget.

Growing tenant demand

Demographic changes, including a growing population (the UK’s population has increased 35% since 1950) and changing preferences (the younger generation is more likely to be a tenant rather than owner as it affords flexibility and mobility), leads to growing tenant demand. Furthermore, during recessionary periods, tenant demand actually tends to accelerate as few individuals take the commitment to purchase their first home. Rental growth in the last 12 months has been 11%, as reported by Zoopla. As a result, most commentators in the property market still expect moderate house price growth over the next five years.

Below we can see an average of circa 3% capital growth per year (see Exhibit 4).

But what about the rapidly increasing mortgage rates we are seeing?

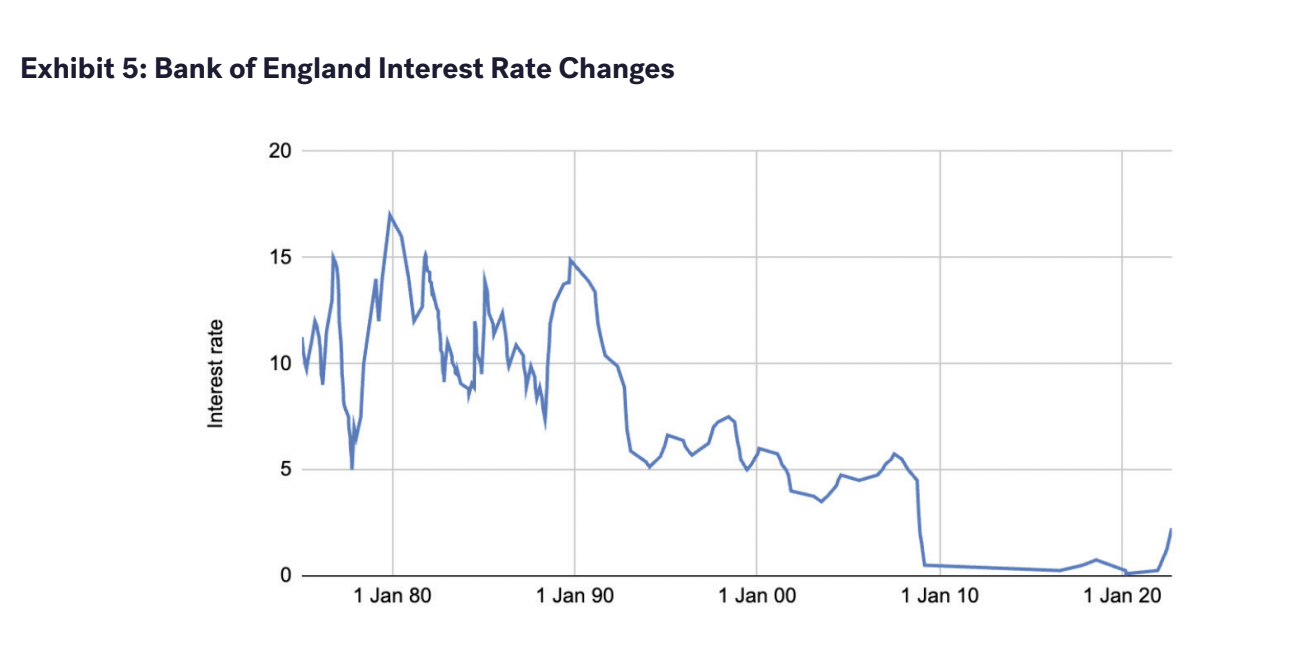

It is important to remember that the last decade of ultra low interest rates is the anomaly (see Exhibit 5). Over the last four decades, and excluding the last decade, the Bank of England’s rate has consistently been above 5%. During those decades there has been a thriving property market.

Savvy investors also realise that although mortgage rates have increased to circa 5%, with inflation at 10% it still means that the real mortgage rate is negative 5%. This is better than free money, lenders are paying borrowers to take their money. Let’s explain that concept. Imagine today a borrower takes out a mortgage of £100k from a bank. Instead of buying a property, they buy apples. Each apple costs £1, so they purchase 100,000 apples. Now let’s imagine that instead of buying apples immediately they waited a year. Inflation was 10% in that year, so an apple now costs £1.10, and so they were only able to buy c.91,000 apples with the same amount of money. The money the bank lent the borrower is worth less in the future because of inflation. So, even with an interest rate of 5%, with an inflation rate of 10%, that money is worth 5% less in a year. Do that long enough and one can literally inflate most of their loan away without paying back a single pound.

So what does this mean for property investors? Well, for those who choose to invest during a more volatile period, the actual cost over time of that borrowing is worth less than during a healthier, lower inflationary period.

Another point to note is that using the right structure to purchase an investment property can shield investors from some of the mortgage rate rises. Using a limited company in the UK to hold investment property means that all mortgage interest is deductible from tax bills. So, every time mortgage interest increases, investors get some of that back with lower tax bills.

Lastly, and perhaps a somewhat obvious point, property investments tend to be long-term investments. The typical property in the UK is only bought or sold once every 20 years. The current mortgage rate increases could be a short-term phenomenon in which case their impact on a 10-20 year investment period is minimal.

However, not all markets are equal. So what strategies could work in this environment?

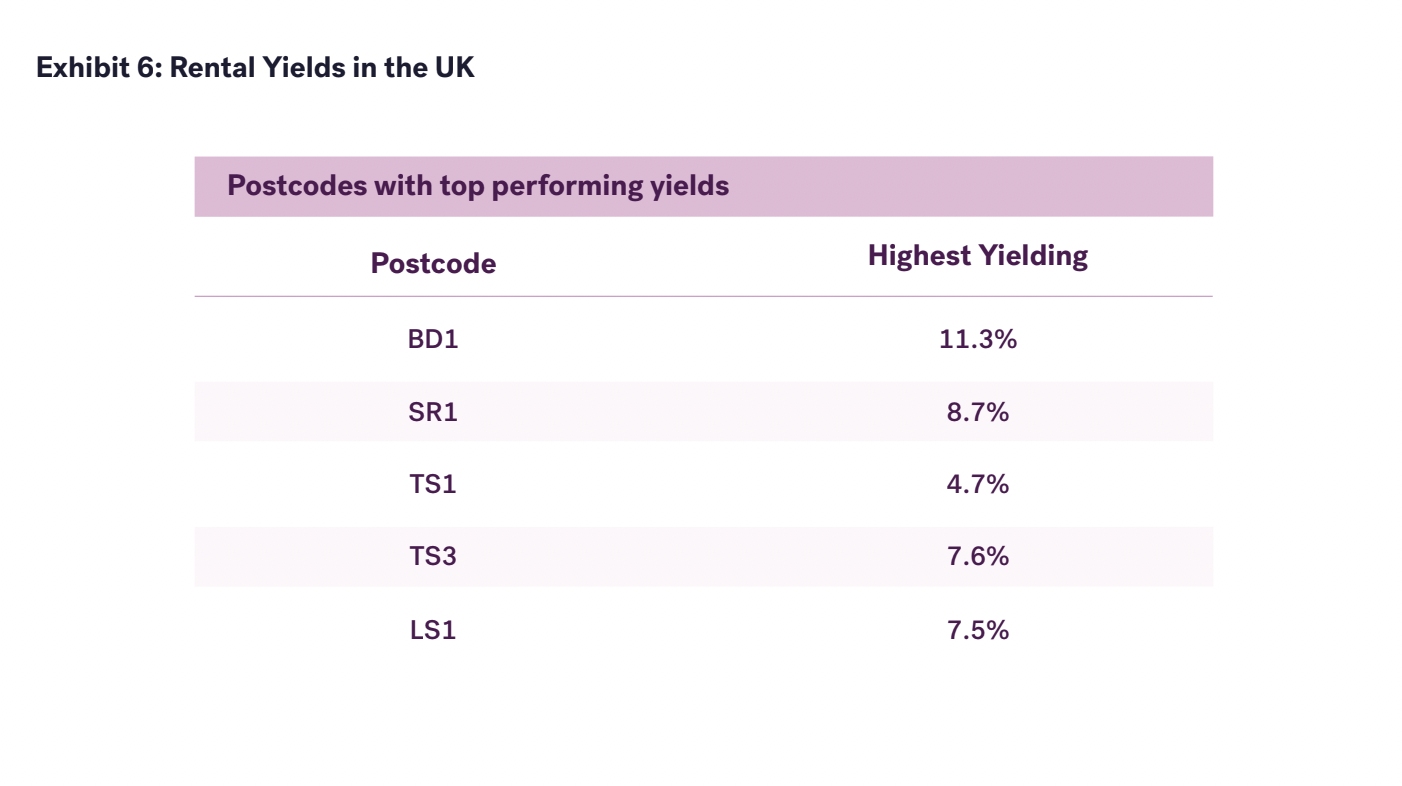

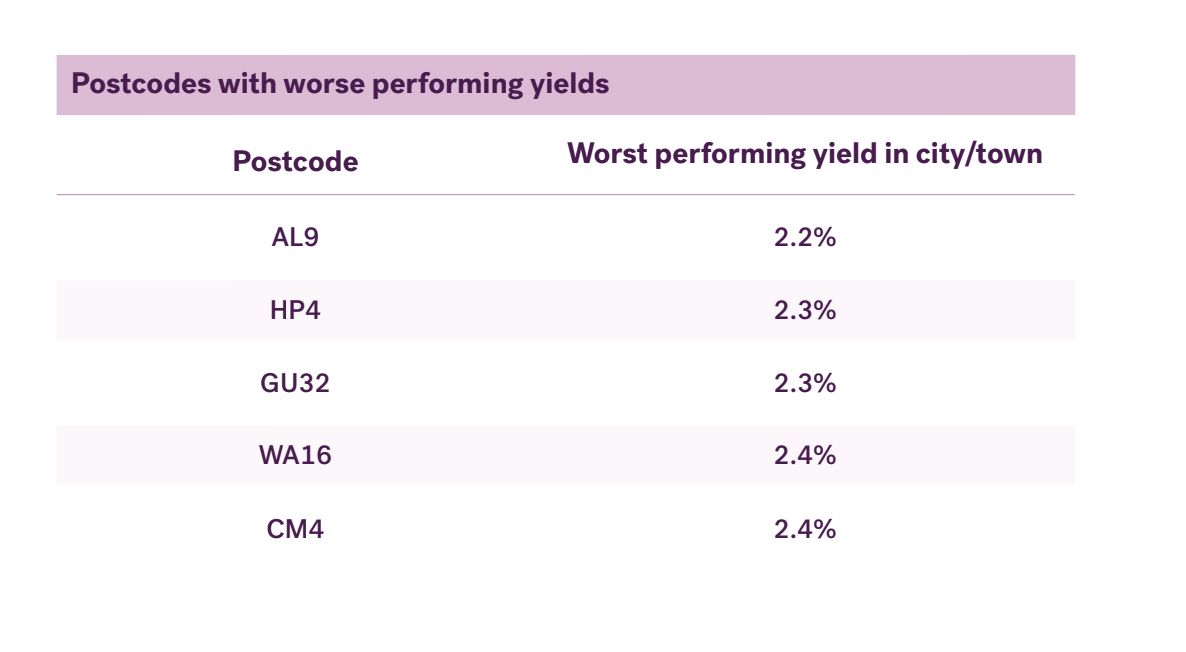

We have already seen a move by investors towards higher yielding properties in order to pay for increasing mortgage interest rates. There is a wide variation in yields across the UK with areas as low as 2.2% (St Albans) to as high as 11.3% (Bradford) (see Exhibit 6).

In addition to regional variations, certain types of properties yield more than others, examples of properties that typically have higher yields include HMOs, holiday lets and short-term lets. There are a number of other strategies to consider:

- Using limited company structures to buy in groups so that a mortgage is not required and the purchase is made entirely with cash.

- Investing in property together also stands to benefit younger investors. In the struggle to protect savings from inflation, buying with peers unlocks a number of investment benefits.

- Those with non-GBP denominated savings purchasing property using the falling value of the GBP to achieve an effective discount on the property purchase.

- Investors taking shorter term debt (2-year fixed mortgages, variable rates without early repayment charges) in order to refinance 1-2 years after purchase.

- Purchasing properties off-plan, which are planned to complete in 18-36 months time to purchase at today’s property prices and obtain financing when the market has hopefully settled.

To conclude...

When all is said and done, volatility in markets creates opportunities for savvy investors. However, navigating these times no doubt requires more experience, more information and greater thought. Perhaps more so than ever before.

With almost 10% market share, 12,000 property investors and over 1,300 partners at GetGround we have a broad, informed view of the property market. Whether you’re looking to invest in UK property (either from the UK or abroad) or to optimise your investments through a limited company structure, we’re here to help.

Get in touch to find out how.

This is for your information only – you shouldn't view this as legal advice, tax advice, investment advice, or any advice at all. While we've tried to make sure this information is accurate and up to date, things can change, so it shouldn't be viewed as totally comprehensive. GetGround always recommends you seek out independent advice before making any investment decisions.

7 February, 2025

The Impact of Interest Rate Drops on UK Property Investors

On February 6th, 2025, the Bank of England announced a reduction in its base interest rate from 4.75% to 4.50%. Although an expected announcement, ...

5 February, 2025

Best Investment Property Locations in 2025: UK Regional Hotspots

The UK property market is becoming increasingly regionalised, with significant differences in growth potential, rental yields, and demand across the ...

5 February, 2025

How Economic Factors Can Impact UK Landlords

Even with the recent volatility of the UK economic market, the UK property market has remained resilient with homeowners and property investors still ...